At 20:00 Beijing time on January 3, according to a CCTV news report, US officials revealed that US President Trump had ordered a military strike against targets in Venezuela. According to reports, the strike lasted about one hour, targeting key facilities including military airports, the Ministry of National Defense building, and ports.

Many people might have gained a deeper understanding of Venezuela for the first time through this news. Although its land area is not particularly large, the country is extremely rich in mineral resources, earning it the nickname "geological treasure."

- Its proven oil reserves amount to 302.8 billion barrels, ranking first in the world. Natural gas reserves stand at 567 million m³, ranking eighth globally.

- Proven bauxite reserves are 1.33 billion mt, placing it third worldwide. Estimated gold reserves are 792 mt, ranking thirteenth globally.

- Additionally, it possesses iron ore resources of 14.6 billion mt, titanium reserves of 39 million mt, diamond reserves of 41 million carats, phosphorite resources of 250 million mt, coal resources of approximately 9 billion mt, and nickel ore reserves of 490,000 mt, among others.

The escalation of this geopolitical conflict is expected to cause fluctuations in the supply-demand patterns of various commodities, including crude oil, natural gas, bauxite, and iron ore. Although Venezuela is not currently a mainstream supplier in the global iron ore trade, its resource potential and geopolitical changes could still exert some influence on related market sentiment and medium to long-term supply expectations.

It is understood that Venezuela's total iron ore reserves amount to 14.657 billion mt, of which proven reserves are 4.184 billion mt. Venezuela's iron ore is primarily located in the Imataca Iron Belt, with deposits being Mesoarchean metamorphic deposits containing hematite and magnetite as the iron minerals. The main deposits are situated in the areas of Piar Municipality and Guayana Municipality in Estado Bolívar State, including Bolívar, San Isidro, Los Barrancos, etc. There are five producing mines around Piar Municipality (Bolívar, San Isidro, Los Barrancos, Altamira, Las Pailas), with proven ore reserves reaching 2.35 billion mt, accounting for 64% of Venezuela's total proven ore reserves.

Venezuela's Location

From a resource reserve perspective, Venezuela's iron ore reserves rank among the top globally, but its mining industry is deeply mired in difficulties, hindered by multiple constraints including politics, economics, infrastructure, and sanctions. Since 2000, the government implemented large-scale nationalization of mineral resources, leading to inefficiencies in state-owned enterprises and a lack of sustained investment in exploration and capacity upgrades. Infrastructure has severely deteriorated, and technological and managerial capabilities are insufficient, with production barely maintained at minimal levels.

Currently, the sole iron ore producer in Venezuela is CVG Ferrominera Orinoco, with an annual capacity of 25 million mt. Since nationalization, the company has long faced funding shortages, and its mining, beneficiation, and other equipment are generally outdated and inefficient. Simultaneously, railway facilities connecting ports and mines are aging, limiting transport capacity. Coupled with nationwide unstable power supply, production at mines and beneficiation plants is frequently interrupted. Against this backdrop of long-term systemic production and operational collapse, the company's iron ore operating rate is only between 10% and 20%. Due to limited domestic consumption, most iron ore is exported, primarily to China, the US, and Western European countries.

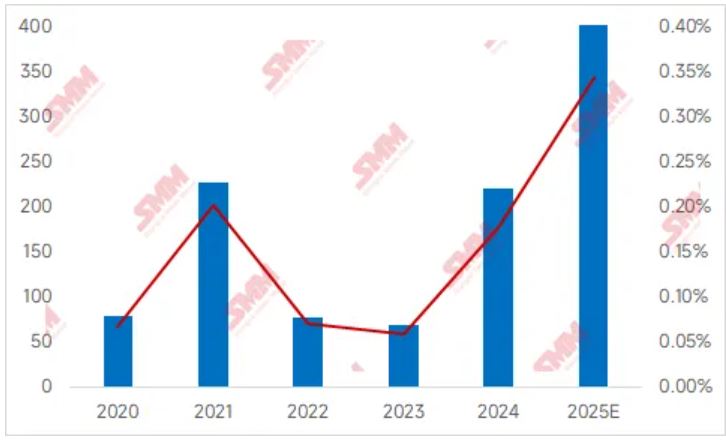

In recent years, with the strengthening of China-Venezuela relations, exports of iron ore to China have gradually increased. Based on SMM's compiled data from the past five years, China's total iron ore imports from Venezuela in 2020 were merely 780,000 mt. Starting in 2024, import volumes showed a significant increase. According to General Administration of Customs statistics, China's imports of Venezuelan iron ore from January to November 2025 totaled 3.81 million mt; combined with SMM's estimate for December port arrivals, the full-year import volume from Venezuela for 2025 is projected to be approximately 4.3 million mt.

Nevertheless, this import volume accounts for only about 0.3% of China's total iron ore imports, a very small proportion. Additionally, the iron ore exported from Venezuela to China is primarily high-grade, with both fines and lumps having an iron content of about 65%. Looking at the current structure of iron ore inventories at Chinese ports, inventories of both high-grade fines and lumps are at high levels.

Therefore, the impact of this geopolitical event on the actual iron ore supply-demand pattern is relatively limited, but it may cause short-term fluctuations in market sentiment. SMM will continue to monitor port arrivals of Venezuelan iron ore. You can log in to the SMM database to view iron ore port departure and arrival data.

China's Imports of Venezuelan Iron Ore and Its Share of Total Imports

Unit: 10kt

Data Source: SMM General Administration of Customs

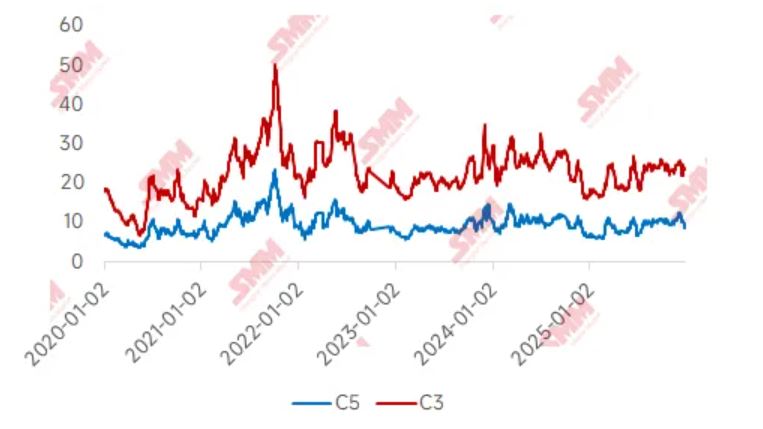

This geopolitical conflict might indirectly affect iron ore costs by pushing up global ocean freight rates. Venezuela possesses the world's largest crude oil reserves, but its current production is only about 1 million barrels per day. The heavy crude oil it produces holds a special position in the global supply chain. If the situation deteriorates, leading to disruptions in oil production and exports, it would directly reduce the supply of heavy crude oil, potentially triggering a short-term rise in international oil prices. As shipping fuel costs are closely linked to international oil prices, an increase in oil prices would be directly transmitted to the shipping industry, raising the operating costs of dry bulk carriers (including Capesize vessels that transport iron ore), which in turn could drive up overall ocean freight rates.

However, the specific magnitude of this impact remains uncertain and highly depends on the actual duration of the conflict, the scope of escalation, and the response measures from other global oil producers (such as OPEC+). SMM will continue to closely monitor how this event evolves in the future to assess its ultimate effect on the shipping market and iron ore CIF costs.

Ocean Freight Rate

Unit: USD/dmt

Sources: SMM, Shanghai Shipping Exchange (SSE)

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)